Are We in a Stock Bubble?

One of the reasons that it is not a good idea to try to time the market is because it is impossible to know when big moves will happen. It is better to stay the course, weather the ups and downs, and focus instead on long term goals.

Source: FactSet, Archer Bay Capital LLC

The chart above shows the performance of the S&P 500 Index since the start of the year. Not much happened during the first two months of the year. It bounced around in an uninspiring way. Then there was a steep climb in part of March and April, and now it has been sort of flat since May.

If you stayed invested the full time, the total return (including dividends) of the S&P 500 since the beginning of the year is 14%. That is a pretty attractive return when the 10-year Treasury bond yield is hovering around 1.5% (for 10 years!?!).

But what is expected for the second half of the year? Since the biggest driver of stock prices is earnings, we watch profit forecasts closely. As usual, there is both good and bad news in the outlook.

More Profit Growth

When we say that we watch profit forecasts closely, we mean that we are looking for changes in Wall Street expectations. In addition, we are comparing the forecasts to the actual results.

We use the S&P 500 companies as a proxy for the US stock market because the market value of those 500 companies represents roughly 73 percent of the value of the total US market. Fortunately, there is a lot of publicly available data on those 500 companies to analyze.

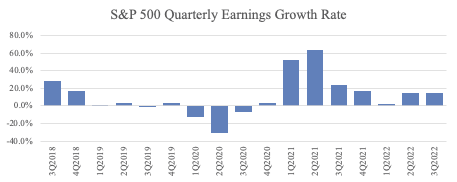

Obviously, 2020 was a rough year for companies. There was a 30 percent decline in earnings in just the second quarter of last year, when the world was at the peak of the shut-down. Because corporate profits last year were so depressed, the year-over-year growth comparison for 2021 looks very strong. This was to be expected.

Source: Thomson Reuters, Refinitiv, Archer Bay Capital LLC

What was not expected was just how strong those profits are. At the beginning of this year, Wall Street analysts were forecasting 23 percent growth in profits for 2021 versus 2020. Given the strong results that companies have delivered so far, that profit growth is now expected to be over 36 percent.

When companies deliver better than expected results, stock prices generally go up…and that is what has fueled the stock performance so far this year. But can it continue?

Preparing for 2022

One worrying trend seen in the S&P 500 Quarterly Earnings Growth Rate chart is the declining growth rate from the second quarter of 2021 through to the first quarter of 2022.

Even though the growth is still positive, a decline in the rate of change usually leads to a market pullback. A 10 percent decline in this environment is not unusual.

This means that someone who was invested at the beginning of the year would still have a positive return, it just isn’t as great as it is right now (but it is still better than the 1.5% Treasury bond yield). But we don’t want to try to time the market and it doesn’t make sense to sell from a tax perspective and pay short term gains.

It also doesn’t make sense to sell because we could be wrong.

One reason why we could be wrong is that there a tremendous amount of cash sitting on the sidelines. We saw this happen in 2009. As the stock market started to recover from the bottom of the Global Financial Crisis, the expected growth of earnings jumped around, especially in the industry at the epicenter of the crisis – the banks. Many investors were skeptical of the recovery and sat on cash waiting for a significant pullback. It didn’t happen. Every time there was a dip in the market, new cash came into stocks and supported the price.

This type of behavior could help support the market this time as well. This is one of those times where we hold our nose and just wait it out because ultimately, earnings growth will surprise again.

With Stocks, We Are Buying Future Earnings

Forget for a second about growth rates and let’s look at actual earnings and expected future earnings.

Source: Thomson Reuters, Refinitiv, Archer Bay Capital LLC*

The Covid-related dip in profits in 2020 is obvious in the above chart, as is the continuation of earnings growth in the coming year. This is the trend that is most important. It is what we base our asset allocation decisions on and our preference for stocks over bonds at this time.

We don’t believe the broad stock market is in a bubble but we do expect volatility.

Since we are at the start of a new business cycle, companies are in their peak time for earnings growth surprises. If you are investing in stocks, do it for the multi-year growth. Don’t try to time the quarterly earnings swings. It isn’t tax efficient and no one can consistently get it right.

At Archer Bay Capital, we help clients better understand the markets and the economy so we can make better financial decisions together. Contact us to discuss stocks, bonds, and our forecast for economic growth, or to schedule a consultation today.