The Debt Ceiling and the Bond Market

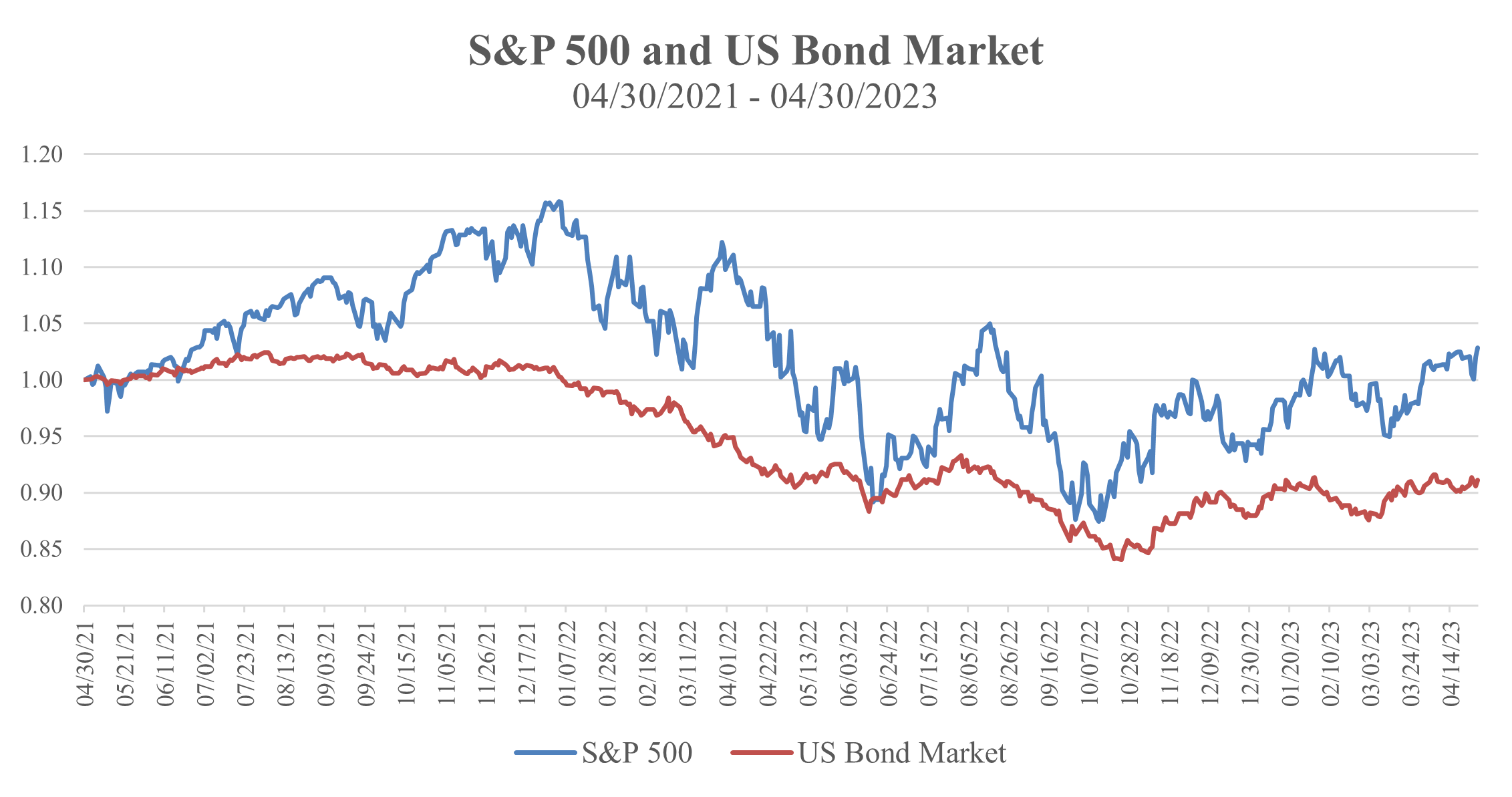

Source: FactSet Research Systems (S&P 500 and the Bloomberg US Bond Aggregate); Archer Bay Capital LLC

It is time once again for Congress and the President to raise the debt ceiling. This process always garners lots of headlines and media attention. At the same time, it has always gotten resolved and then the process repeats again and again.

Debt limits started during World War I when Congress passed legislation to allow it to issue debt to finance the US participation in the war. Now it is used to give lawmakers a chance to vocalize their own agendas regarding budgets and spending priorities.

Since US Treasury debt is widely considered to be the safest in the world, it behooves Congress and the President to ensure that this remains true, but how we get there can often be a journey.

Where We Stand Today

In January of this year, the government technically ran out of money and is unable to raise additional debt to cover its expenses. The US Treasury has been employing ‘extraordinary measures’ to continue paying the bills. How long this can last can be difficult to estimate; it depends on how much the government is receiving in taxes as well as some other considerations. Many government budget watchers believe that sometime between June and September the Treasury will run out of options and money

Last Friday, the House of Representatives passed a bill to raise the debt ceiling which included significant cuts to government spending. At this point, the bill passed by the Republican-controlled House is very unlikely to be passed by either the Democratic-controlled Senate or the President. However, it is considered to be the first step toward negotiations.

What makes the negotiation trickier this year is a challenging economy – persistently high inflation, recent bank failures, and increasing rates -- and the continued polarization of the political parties. This is a particularly delicate time to play political games.

The government is obligated to pay its debts. The Fourteenth Amendment states that “The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned….”

While we believe that ultimately the debts will be paid, there is a risk of a delay of payments while Congress and the President hammer this out.

Bond Market Reaction

We are already seeing the impact of this in the bond markets. Traditionally, bonds that mature in the near-term have lower yields than bonds that mature later. The longer the time period until maturity, the higher the risk that the yield is unattractive; investors demand more compensation for that risk and yields are higher.

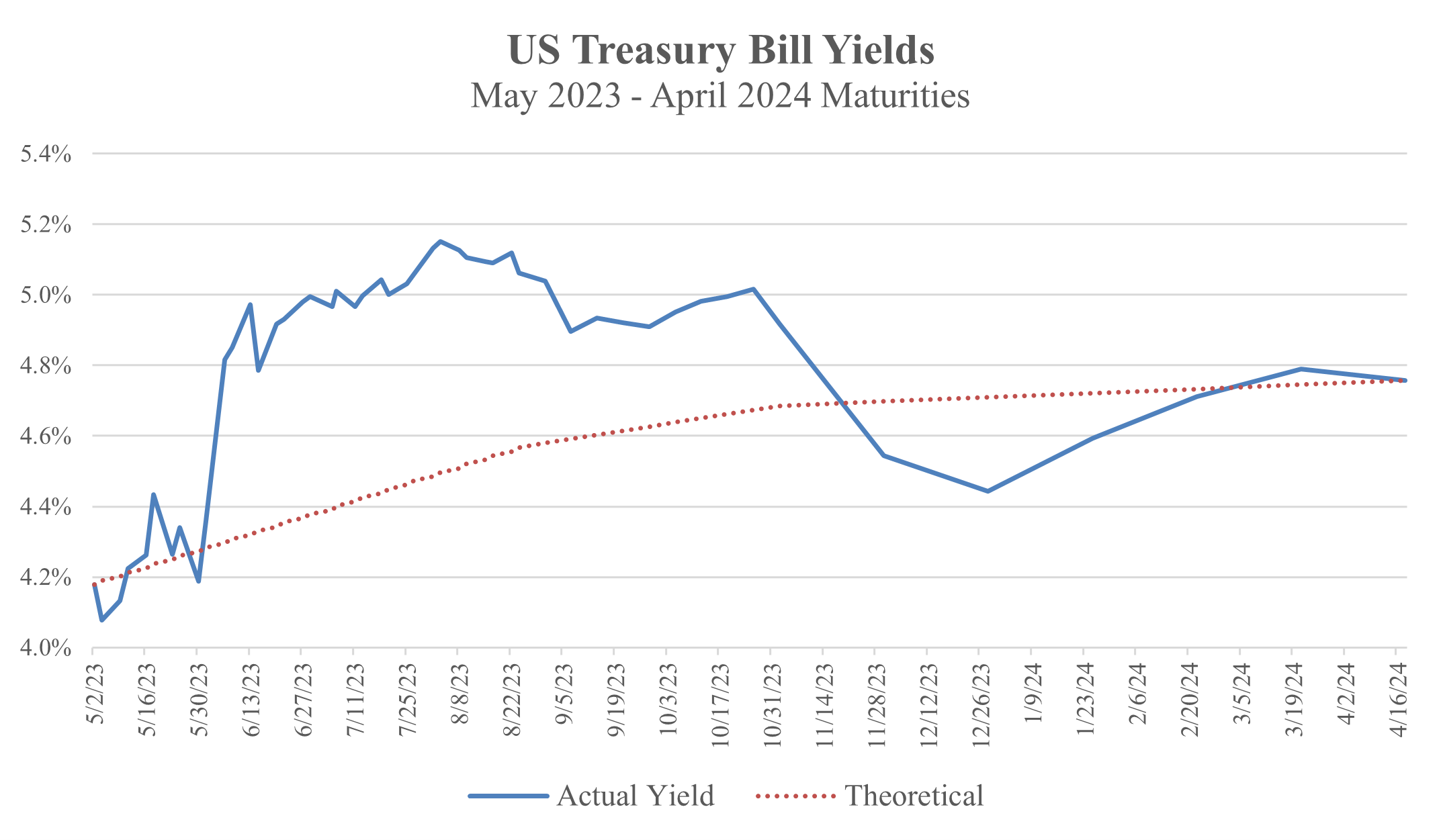

Source: Fidelity Investments 4/30/2023; Archer Bay Capital LLC

In the graph above, the blue line represents the current yields on short-term US Treasury Bills that mature between now and a year from now. Because the bond market is concerned about a potential default, there is an increase in yields beginning this month from 4.1% to over 5.0%.

We have included the ‘theoretical’ yield, represented by a dotted red line, to show what the yield curve would look like in more normal times. As you can see, this is a highly unusual pattern for Treasury yields and it is being driven by these concerns about the debt ceiling.

While it is impossible to predict the ups and downs of the debt ceiling negotiations (and their near-term impact on the markets), the bond markets are signaling that they expect both Congress and the President to compromise on a bill that will continue funding the government by the fall – which is reflected by the decline in yields after October.

We also believe that no one in Congress ultimately wants to jeopardize the full faith and credit of US as the most reliable borrower in the world. It doesn’t mean that we won’t see a lot of headlines about it in the meantime as the terms are hashed out.

Stock Market Response

The stock market has been more focused on the banking crisis than on the government debt ceiling. Despite the takeover of four banks in the past two months (Silicon Valley Bank, Signature Bank, Credit Suisse, and First Republic Bank), financial stocks overall are expected to have good earnings growth this year.

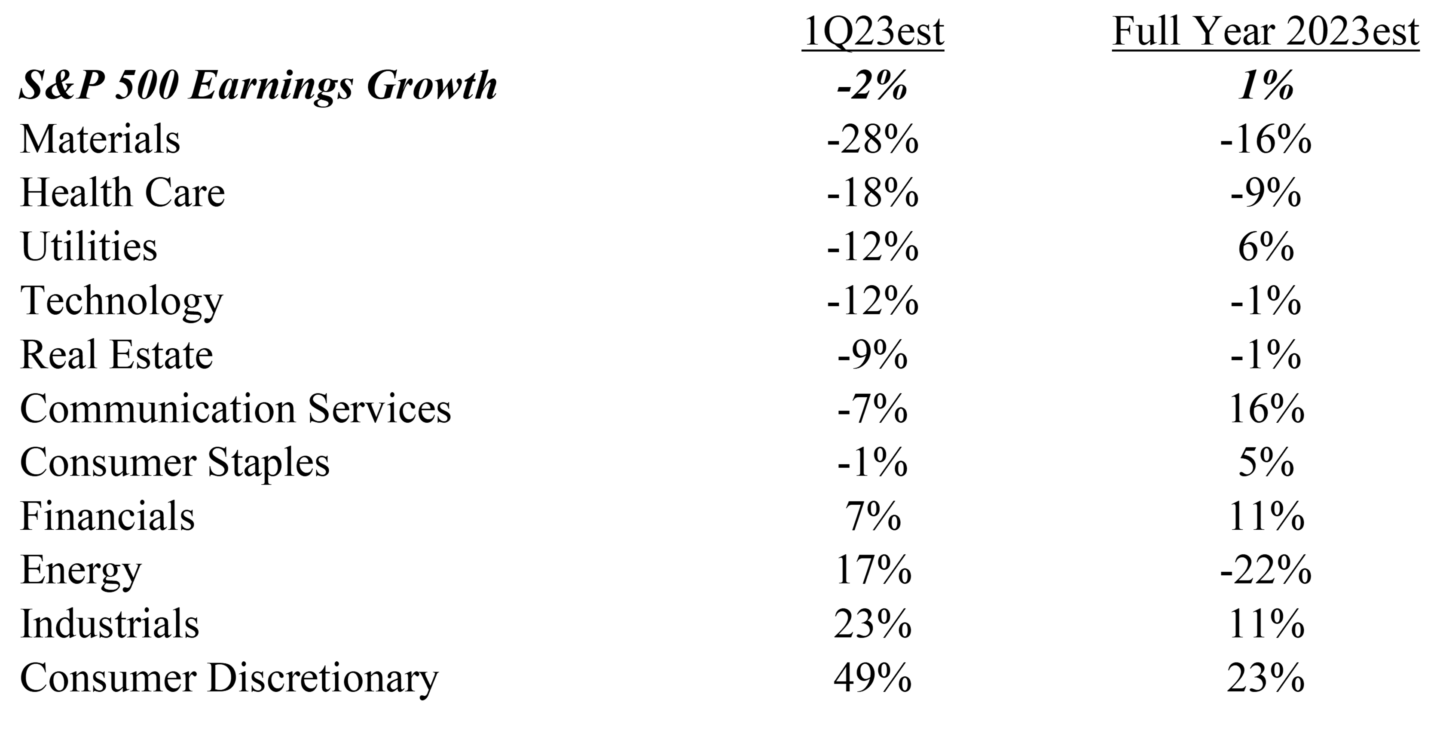

Here is a breakdown of profit forecasts by industry sector in the S&P 500 ranked by earnings growth rate.

Source: Refinitiv, 04/28/2023, Archer Bay Capital LLC

Profits in the first quarter for the S&P 500 companies, in aggregate, were below the level of profits last year, but earnings are expected to recover to slightly positive growth by the end of the year.

But this doesn’t apply to all industries. Some industries, such as Energy, Materials and Health Care are expected to have lower earnings this year. Technology and Real Estate are expected to be slightly down for the year. Surprisingly, the Financials sector delivered 7% profit growth last quarter and is expected to have 11% growth for the full year. The media hasn’t been reporting that good news.

Our conclusion is that the debt ceiling has less to do with stocks and corporate profitability than it does the short-term Treasury bond market. We do expect political scare tactics to create volatility more broadly, in both stocks and bonds, but that it is not an event that changes the outlook for profits.