Earnings, Recession Fear, and Banks

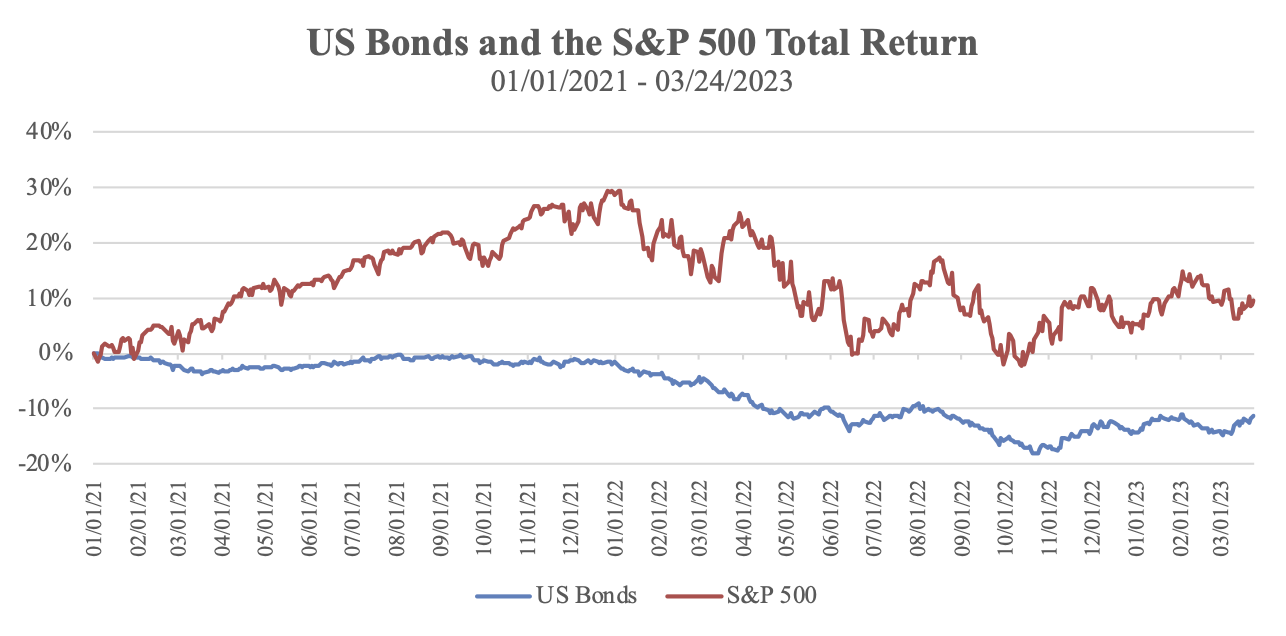

Source: FactSet Research; Archer Bay Capital LLC (US Bonds = Bloomberg Bond Aggregate Index)

The past year and a half have been a tough time in both the bond and the stock market. The S&P 500 has been bouncing around the current level since last May. And rising interest rates have hurt the bond market even more than stocks.

We believe that the market bottomed last October when investor pessimism peaked. At that point, the Federal Reserve still had two big rate increases ahead and inflation was above 8%.

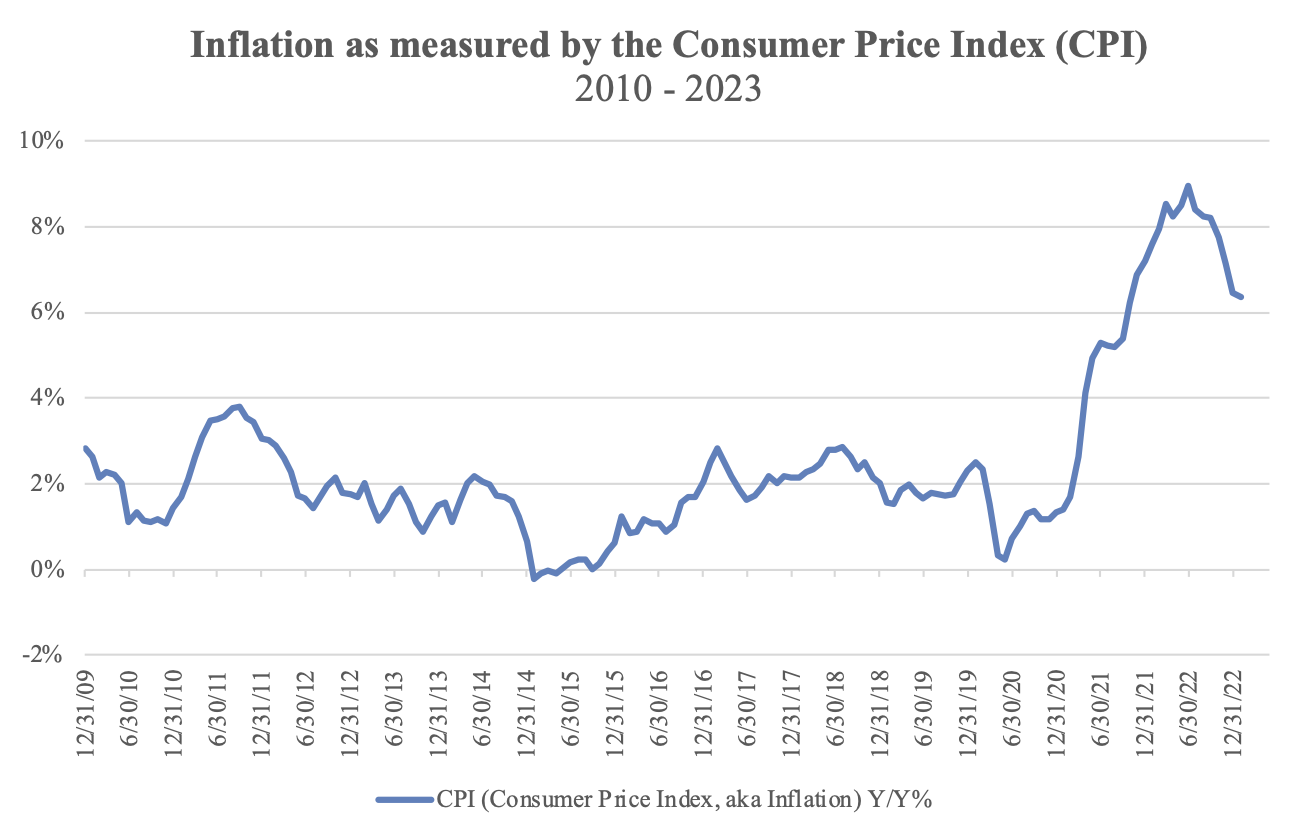

The latest inflation report showed Consumer Price Index (CPI) nearing 6% and there is some expectation that the Federal Reserve may pause raising rates soon.

Source: Bureau of Labor Statistics; FactSet Research Systems; Archer Bay Capital LLC

As interest rates are rising and inflation is coming down, there is the fear that the economy will be slowing to the point of recession. We think the slowdown is already here and we can see evidence of it in corporate results.

Recession in 2023?

One definition of recession is when the economy has two consecutive quarters of declining Gross Domestic Product (GDP), AND the government has to officially declare it a recession.

During the pandemic year of 2020, the US only had one quarter when GDP declined, but it was extreme and the National Bureau of Economic Research (NBER) did declare it a recession. In 2022, the US had two consecutive quarters of negative GDP growth in the first and second quarter but the government didn’t call it a recession.

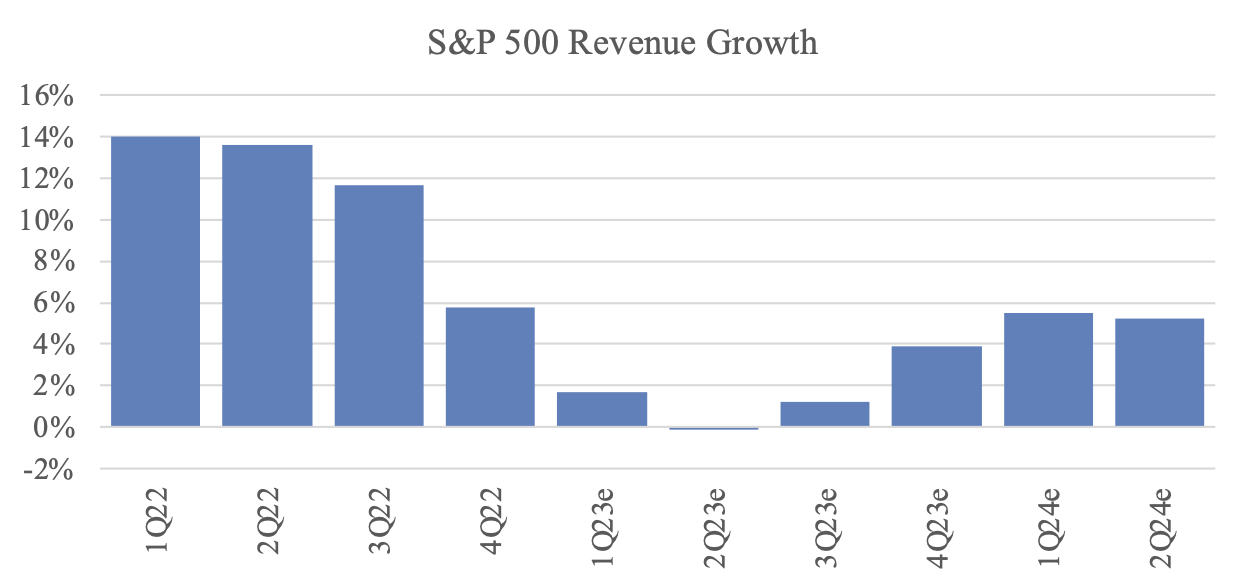

Companies were definitely feeling the squeeze in 2022. It was reflected in declining revenue growth and profit margin pressure. The most recent Wall Street estimates are forecasting revenue growth to bottom in the next few months.

Source: Refinitiv, Archer Bay Capital LLC

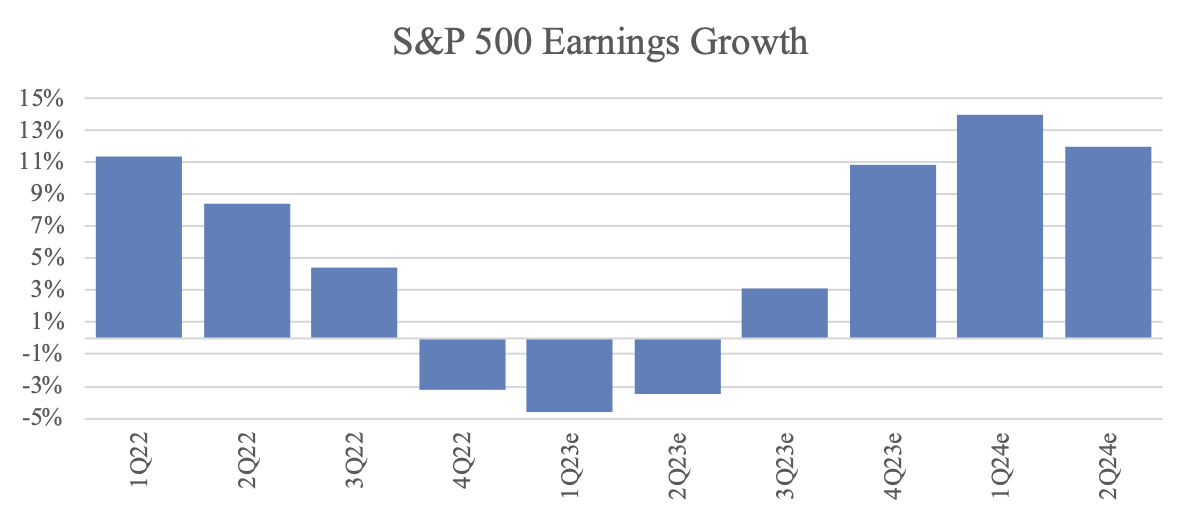

But while revenue is slowing, the corporate earnings decline has already happened, based on what companies have reported from the fourth quarter. The latest Wall Street estimates suggest that the profit decline will bottom this quarter and growth will resume in the second half of this year.

Source: Refinitiv; Archer Bay Capital LLC

Companies have managed through a tough 2022 and look poised to resume growth this year, even if it is modest growth. We will be looking for any changes to these expectations over the next quarter and heading into the summer.

If the earnings forecasts are accurate, then the stock market has been through the worst already. But the banks have certainly given us a scare.

The 2008 Financial Crisis vs the 1980s Savings & Loan Crisis vs Today

During the 2008 Global Financial Crisis, the fear in the financial markets was palpable. Bad loans were the cause of the banking crisis at the time and investors feared what was unknown on the balance sheets of lenders.

Back then, the value of underlying assets and collateral fell below the value of the loans, and poor credit standards meant that many borrowers weren’t able or willing to pay the banks back.

Today, the bank run that caused the failure of Silicon Valley Bank is not related to bad loans. Rather it is a timing mismatch of short-term deposits and longer-term investments that had fallen in value due to higher interest rates.

The current situation with the banks has greater similarity to the Savings and Loan (S&L) Crisis[i] of the 1980s than the 2008 Global Financial Crisis. Through the 1970s and into the early 1980s, interest rates were rising as inflation picked up. This created a mismatch between the rates charged by banks for loans and the rates demanded by depositors. Poor regulatory oversight allowed the problem to fester for multiple years.

Bank runs occurred at stressed institutions and over a thousand S&L institutions were closed by regulators in the 1980s and early 1990s[ii]. Ultimately, the government bailout them out. The Resolution Trust Company (RTC) was created to unwind these institutions, which helped resolve the crisis. The RTC itself was dissolved in 1994 once reforms were completed.

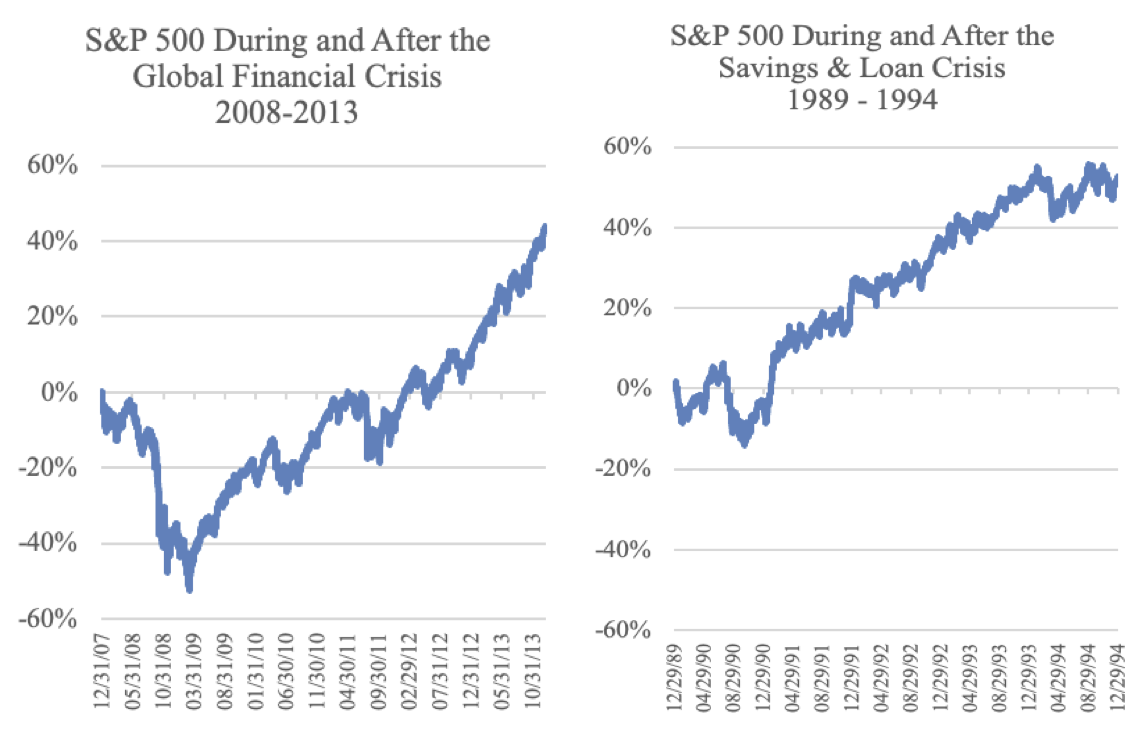

Here is how the S&P 500 performed during the Global Financial Crisis (2008-2013) and the S&L Crisis (1989-1994):

Source: FactSet Research Systems; Archer Bay Capital LLC

The magnitude of the decline was much larger for the 2008 Financial Crisis. After both periods, the stock market saw a multi-year rally.

It is de-stabilizing when financial institutions fail which is why bank regulators around the world try to act quickly when cracks appear. The business model of banks is one that is highly leveraged, which makes them vulnerable to shocks. This is the reason that they are highly regulated to begin with.

There is Always Near-Term Uncertainty

We are unsure if there are other stresses in the financial system right now that have not yet surfaced. Most crises are unpredictable – if people knew about them in advance, they likely wouldn’t happen in the first place.

While investors periodically go through waves of fear and greed, the markets are resilient. We believe that by having a diversified portfolio of stocks and a laddered maturity of high-quality bonds, the portfolios are well positioned to weather the storms.

Please let us know if you have any questions and would like to discuss in greater detail.

At Archer Bay Capital, we help clients better understand the markets and the economy so we can make better financial decisions together. Contact us to discuss stocks, bonds, and our forecast for economic growth, or to schedule a consultation today.