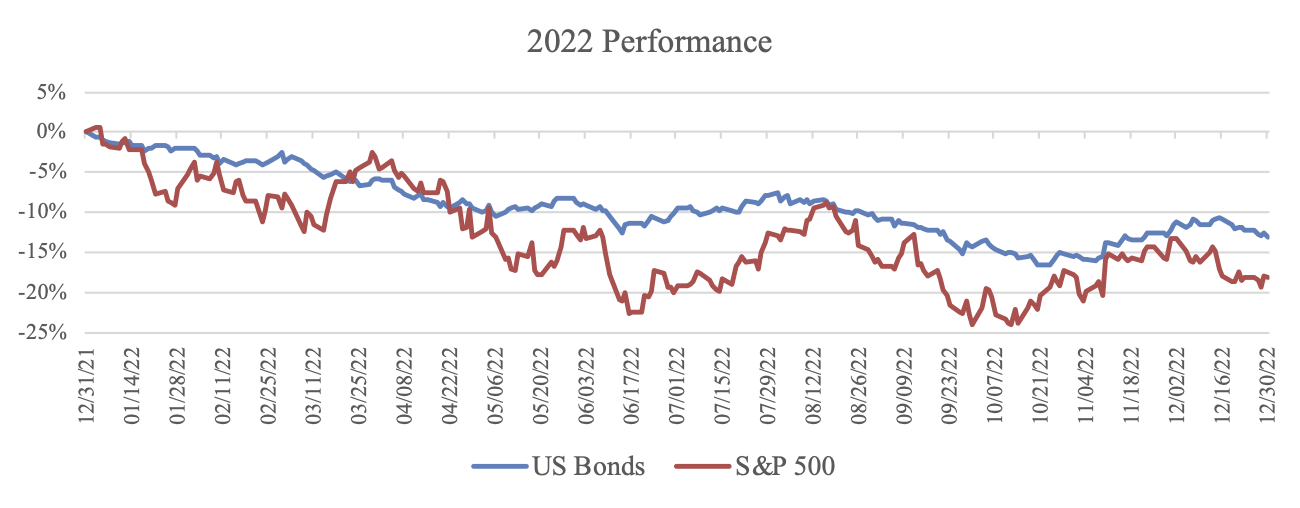

Goodbye 2022 … Glad to be in 2023

In most of our reports we tend to focus on the future, but the past year was so unusual that it is worth reviewing what happened. Both the bond and stock market were down double-digits.

The last time that both markets were down in the same year was in 1969.

Source: FactSet Research, Archer Bay Capital LLC; (Bloomberg Aggregate Bond Index, S&P 500 Total Return)

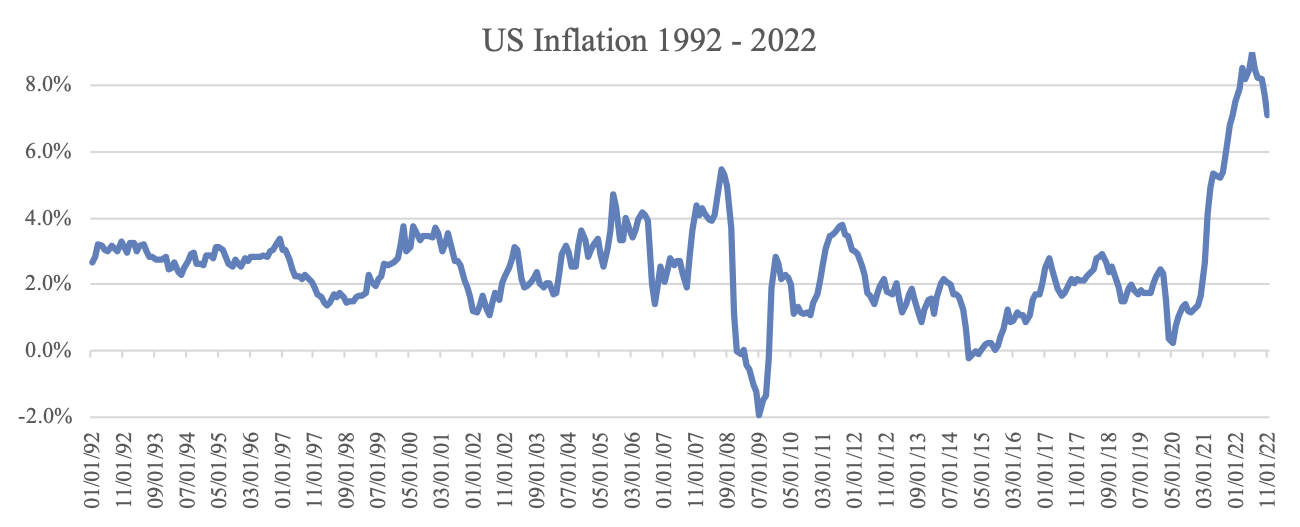

Last year was difficult across most major financial markets. One of the key factors was high inflation. This had a particularly negative effect on the bond markets as the Federal Reserve raised interest rates at a rapid pace in order to halt it. This is quite a reversal from the recent past.

For the past thirty years inflation has been moderate. There have been three periods since the 2008 Global Financial Crisis when inflation was at or even below zero. There were concerns among many economists that deflation was a bigger threat than inflation…until 2021.

Inflation Is Back

Source: FactSet Research (CPI: Consumer Price Index), US Bureau of Labor Statistics; Archer Bay Capital LLC

Due to a combination of government stimulus spending from the pandemic, Covid-related supply chain disruptions, very low interest rates, and pent-up consumer demand, inflation surpassed the Federal Reserve’s 2% target in March 2021 and never looked back.

Inflation reached 7% by the end of 2021. When Russia invaded Ukraine in February 2022, the subsequent spike in food and oil prices pushed inflation above 8%.

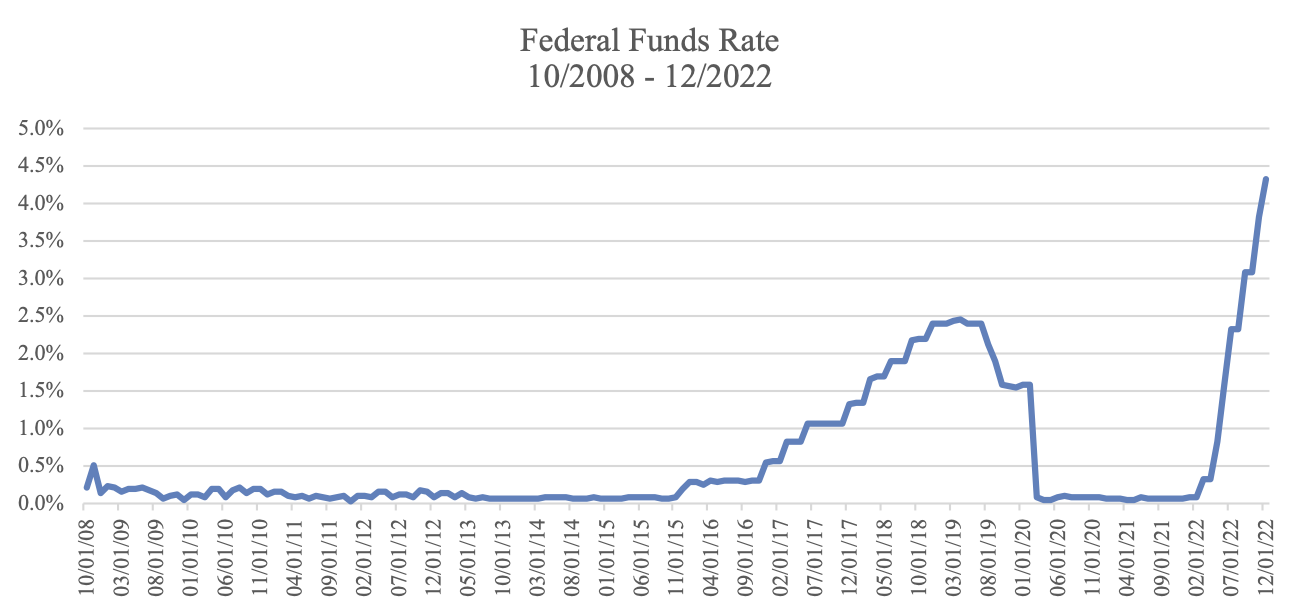

The Fed’s Response

In response, the Federal Reserve began increasing interest rates in March 2022.

Source: FactSet Research, Archer Bay Capital LLC

Higher interest rates are expected to slow economic activity because they make borrowing money more expensive. This will frequently have a direct impact on consumer and business debt, including mortgages, car loans and business loans. Higher borrowing costs can have a ripple effect on the economy and lower overall demand. It is a difficult balancing act because if the economy slows too much, it can fall into recession.

But the bigger risk is that inflation becomes imbedded in the economy, as it did in the 1970s. This is why we expect that the Fed will continue increasing interest rates until we see additional declines in inflation.

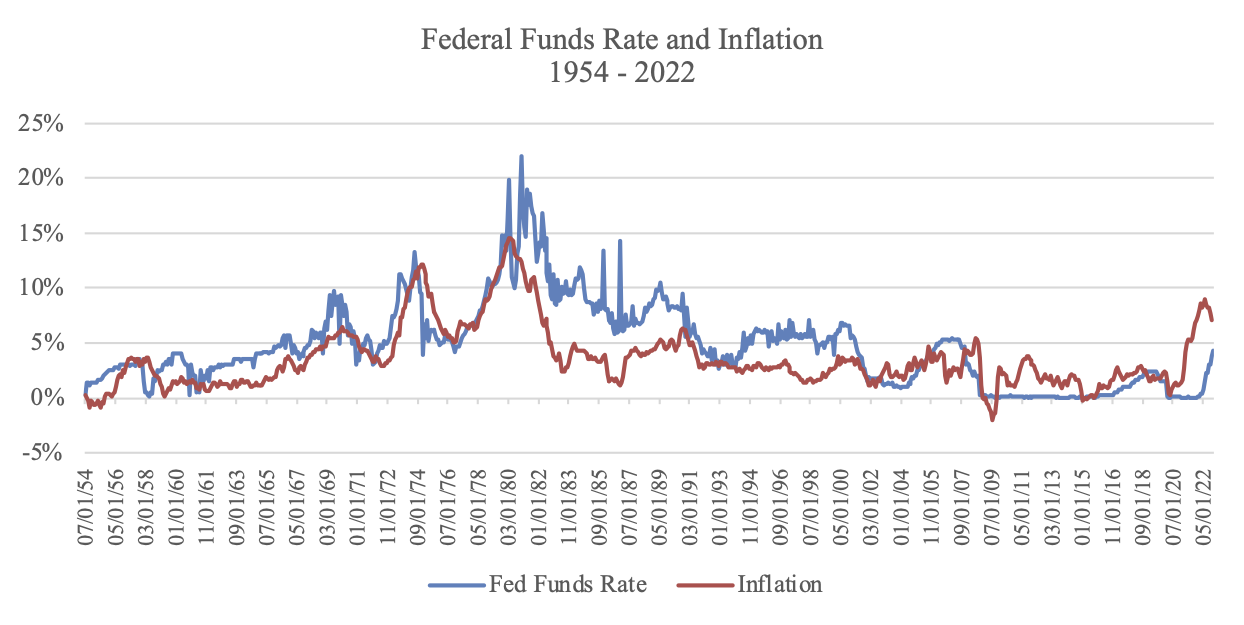

Recalling the 1970s

With two oil shocks (the OPEC oil embargo in 1973 and the Iranian Revolution in 1979), the end of the gold standard for the US dollar, labor strikes for higher pay, and price controls instituted by then-President Nixon, inflation was difficult for many American families and businesses to manage.

Source: FactSet Research; US Bureau of Labor Statistics, St. Louis Federal Reserve https://fred.stlouisfed.org/series/FEDFUNDS; Archer Bay Capital LLC

To get it under control, the Federal Reserve increased the Federal Funds Rate to a whopping 22% in December 1980. It caused a severe recession but succeeded in bringing inflation down.

Today’s Federal Reserve wants to avoid a repeat of the 1970s inflation buildup.

Following the last Fed meeting in December, the Federal Reserve Chairman stated that they will continue to raise rates until it is evident that inflation is under control. They are expected to raise rates again this year, to 5%, and we believe that it could go higher if inflation does not come down.

From a historical perspective, the Federal Funds rate at 4-5% is not extreme, but it feels shocking when rates have been so low for so long.

The response in the bond market is interesting.

Yield Curve Inversion

Fidelity Investments (January 3, 2023), Archer Bay Capital LLC

When the yield for shorter maturity bonds are higher than the yield for longer maturity bonds, it is called an inverted yield curve. This is currently happening in the bond market.

The yield for a US Treasury bill maturing in one-year is higher than the yield for a US Treasury bond that matures in 2-years, 3-years, 5-years, or even 10-years.

When interest rates are lower further in the future than in the near-term, it suggests that bond market investors are less worried about high inflation in ten years, but more worried about what could be happening in two years.

The Fed needs to stick to its plan to ensure that inflation is brought down.

What We Expect In 2023

Inflation is still our biggest concern for 2023. If higher interest rates do cause a recession but they bring inflation back to the lower single digits, we believe that is better than risking a 1970s-like inflation scenario.

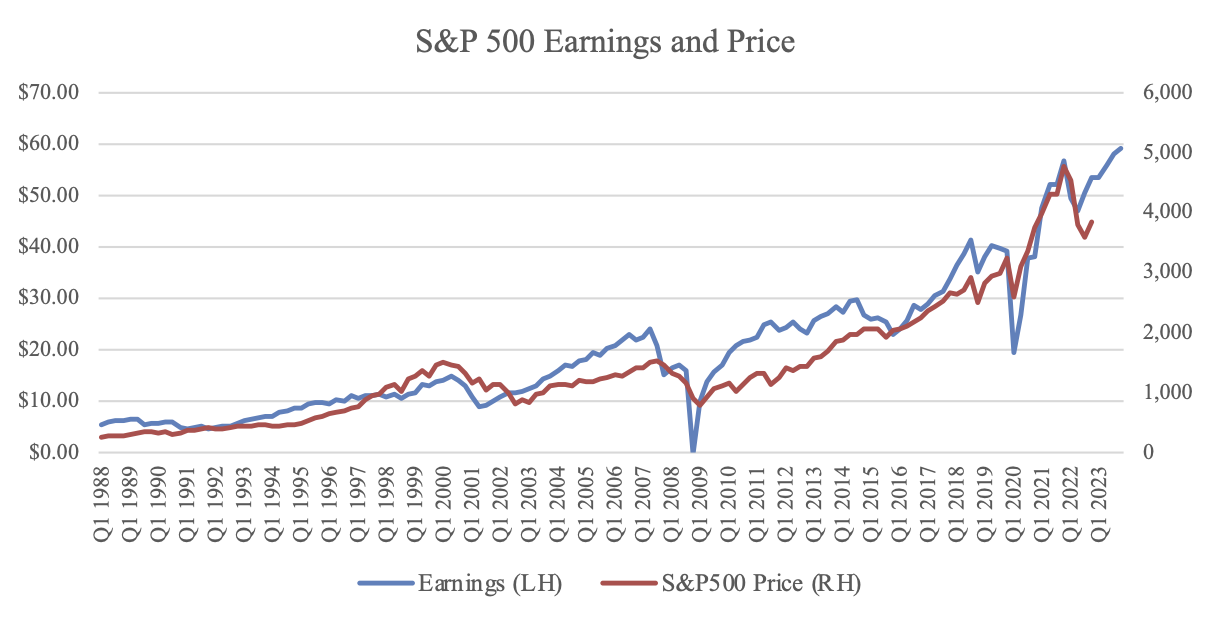

For stocks, we follow the earnings trend and, so far, company profits overall are still expected to grow in 2023, which could bode well for stock prices. We will be watching earnings reports closely later this month for more guidance.

Source: S&P Global https://www.spglobal.com/spdji/en/documents/additional-material/sp-500-eps-est.xlsx; Archer Bay Capital LLC

If Wall Street expectations are wrong and earnings decline, it is clear from the chart that we’ve seen it before. The recessions of 2002, 2008 and 2020 each had significant pullbacks, followed by a healthy recovery each time.

We don’t think the next recession will be different, whether it happens in 2023 or some other point in the future. The problem for investor performance is if they are out of the market during the early rally, then lower returns are the result.

Terri

At Archer Bay Capital, we help clients better understand the markets and the economy so we can make better financial decisions together. Contact us to discuss stocks, bonds, and our forecast for economic growth, or to schedule a consultation today