Inflation, Bond Yields, and the Stock Market

Source: US Bureau of Economic Analysis; FactSet; Archer Bay Capital LLC

The stock market usually gets all of the news headlines but the economy is much more dependent upon the bond market. And the bond market is currently not normal.

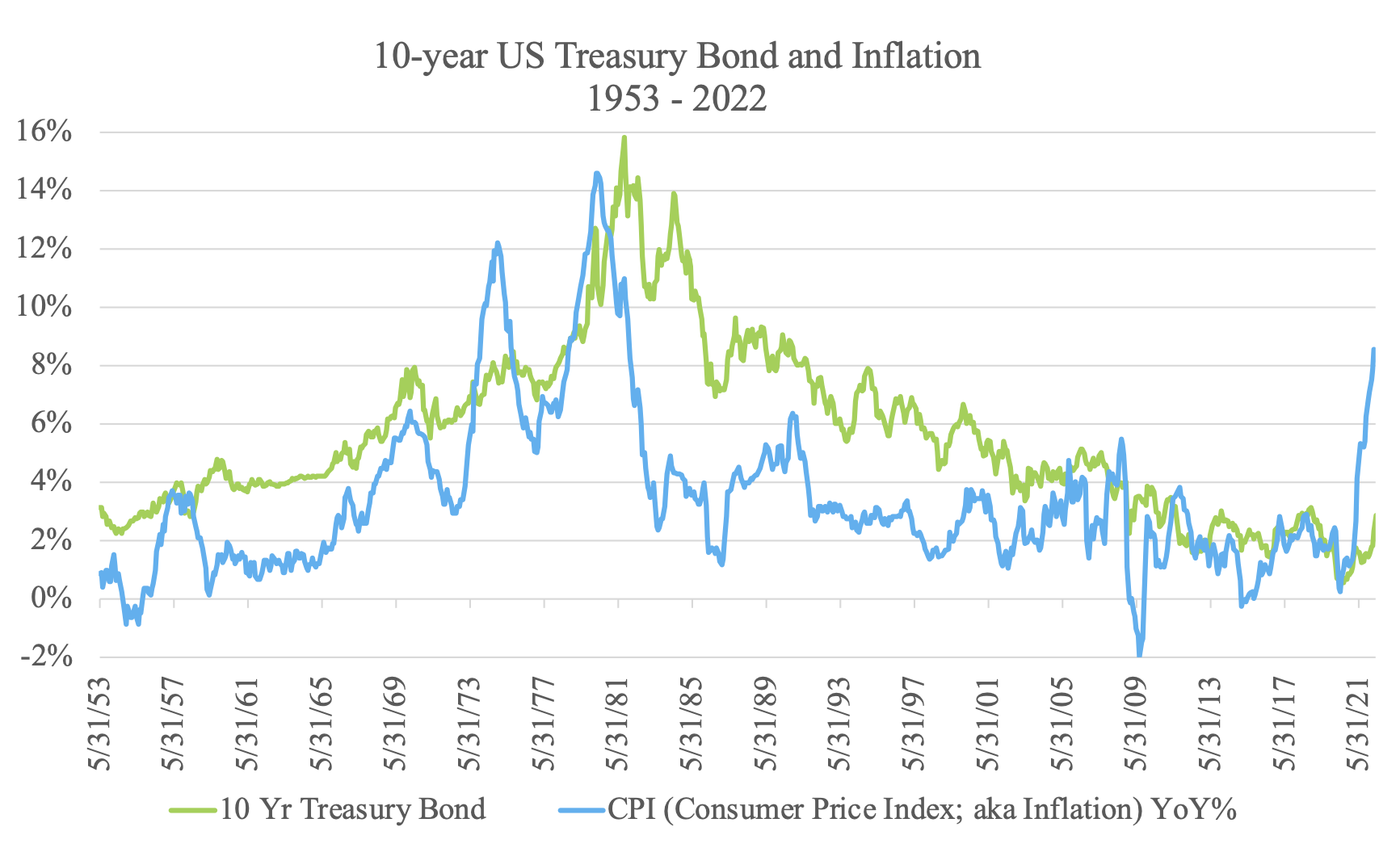

The chart above shows the relationship between inflation and bond yields. In the past seventy years, there have been only three times that inflation was well above bond yields. We are living through one of those periods now.

In order for equilibrium to return, bond yields will have to go up and inflation will have to come down. The existing gap is unsustainable. Be prepared for higher rates.

The Federal Reserve is expected to announce a half a percentage point interest rate increase on Wednesday, June 15th. There is another half a percentage point increase expected in late July. Even after these two rate increases, yields will still be too low.

Consider the facts:

Current overnight Fed funds rate = 0.8%

After two increases in June and July = 0.8% + 0.5% + 0.5% = 1.8%

Yield on the 10-year Treasury bond = 3.1%

Latest inflation measure for May = 8.6%

The gap between the 10-year Treasury yield and inflation = 5.5%

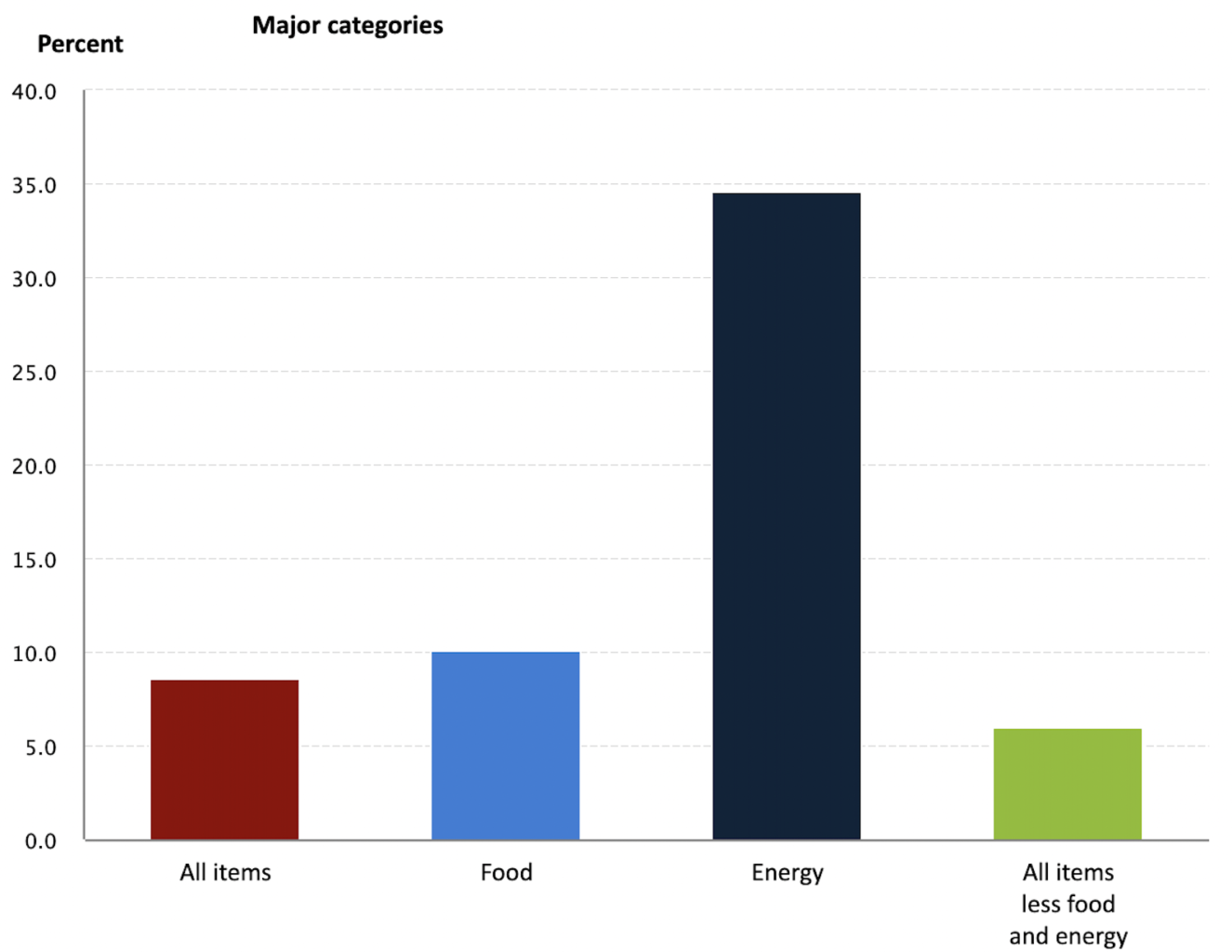

Why is inflation so high and when will it come down?

Source: US Bureau of Labor Statistics; Archer Bay Capital LLC

Energy prices are 35% higher this year versus last year because there is a supply/demand imbalance. There is higher demand as consumers drive more and there is lower supply, from both less drilling and the boycott of Russian oil, which has led to an extremely tight market.

Food prices, housing prices and continued supply chain disruptions have all contributed to inflation. Unfortunately, there isn’t obvious relief coming soon in any of these areas.

The large year-over-year increases should slow once we catch up to price spikes at the end of last year, but prices may not actually decline. In order for inflation to moderate, supply needs to catch up to demand, or demand needs to drop, or some combination of both.

What happens to the stock market?

Source: Standard & Poor’s; Refinitiv; Archer Bay Capital LLC

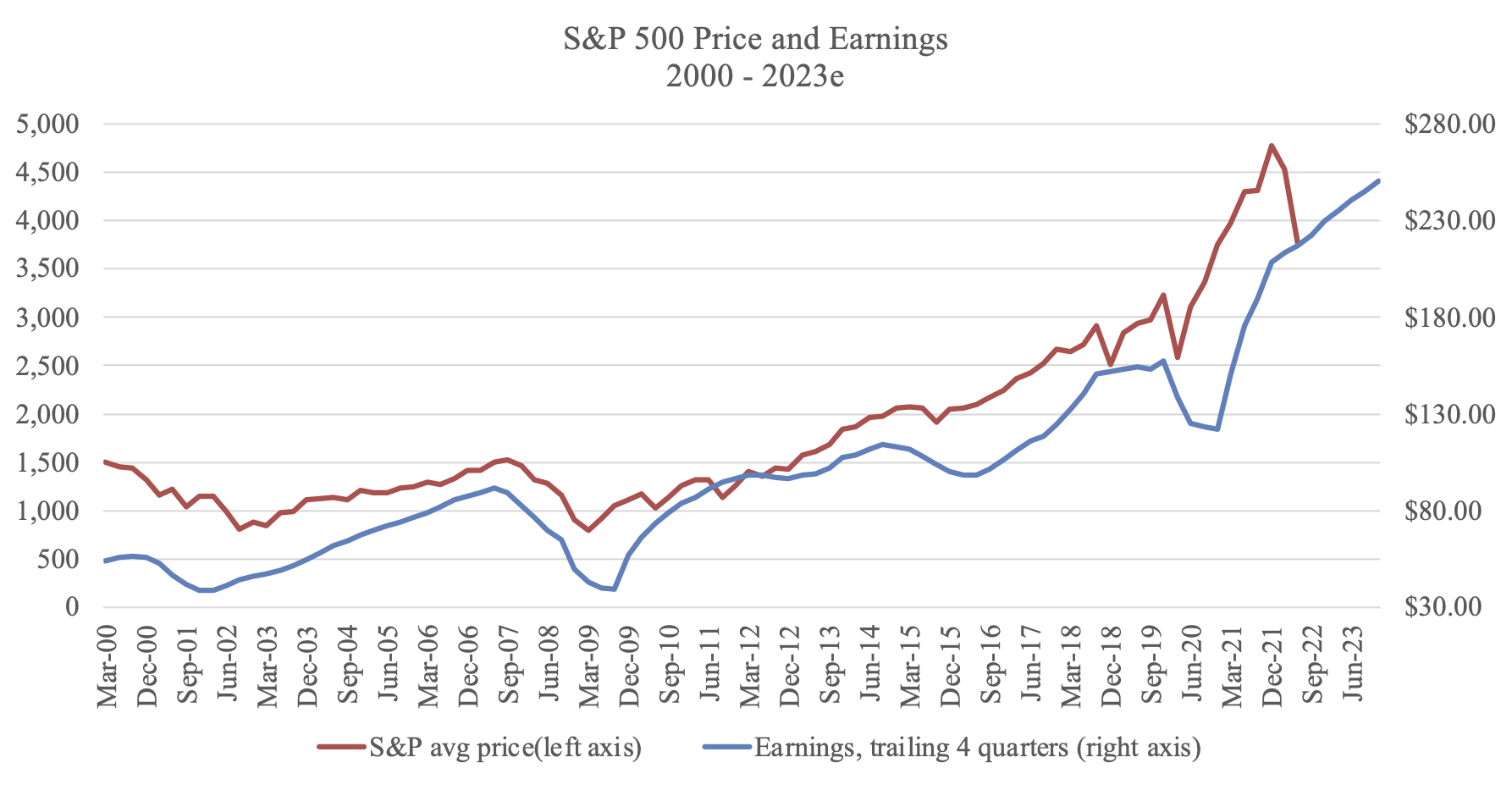

Corporate earnings are highly correlated with stock prices. We are in an unusual period when profits are increasing but stock prices are down. Wall Street earnings forecasts are positive for the rest of 2022 and 2023.

Revenues are growing faster than earnings, which means that profit margins are under pressure. But overall earnings are still growing. If earnings are up, why are prices down?

Our view is that the uncertainty in the bond market is the key overhang in the stock market. Investors want to see inflation moderate and bond yields to return to equilibrium. If interest rates increase too much, the economy will likely go into recession. This is what investors fear and the cause of the sell-off.

Should we make changes to our investments?

The risk with trying to time the entry and exit to the market is, first, it is impossible to pick the bottom to buy or pick the top to sell, and second, the markets move faster than you can trade.

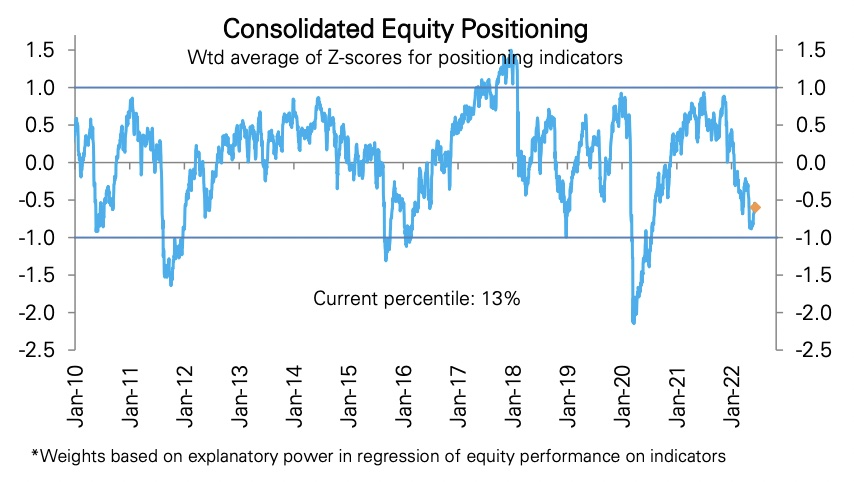

The chart below is a common measure of oversold/overbought positioning in the stock market going back to January 2010. The market is currently near the low end of the range, which means that there are more sellers in the market than buyers. We frequently experience rapid reversals in the market when this indicator hits -1 or +1.

Source: CFTC; Deutsche Bank; Bloomberg Finance; Haver; Archer Bay Capital LLC

There is $4.5 trillion sitting in money market funds which means that there is a lot of cash that could flood back into stocks. We do not want to be out of the market when this happens. Therefore, the answer is no, we should not make changes to our investments.

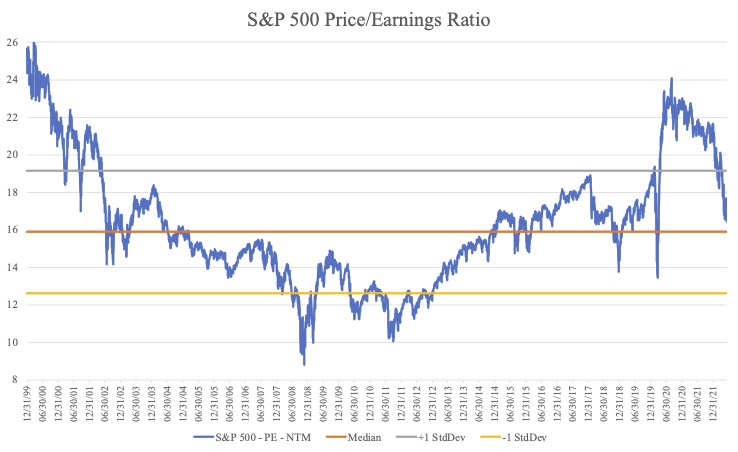

Are valuations cheap?

The Price to Earnings ratio is a common measure of stock valuation. There have been large swings in the ratio over time. Even during the last two years of the pandemic, the stock market swung from a cheap valuation (March 2020) to high valuation (December 2020) to a moderate valuation (today).

Source: FactSet; Refinitiv; Archer Bay Capital LLC

When stock prices decline (numerator), and earnings increase (denominator), the ratio itself declines. This is what has happened this year. In contrast, from 2002 to 2007, both earnings and stock prices were up, but earnings grew faster than stock prices, so the ratio was down. It is possible for the P/E ratio to decline and stock prices to rise.

At the Price/Earnings low in 2008, it was difficult to see the buying opportunity because the economy was in recession and uncertainty was extremely high. Extreme investor fear is what made the market especially cheap.

Applied to today, the market will look cheap if the ratio drops to 14 and earnings are stable. The market could also bounce from current levels, given the high cash level in the system and growing profits.

It feels awful when the markets are down and it also feels awful to miss the rally when the market bounces back. This is why we focus on tracking earnings, because prices eventually follow.

Please let us know if you would like to discuss in greater detail -- we are always happy to share more in-depth research.