Is the Stock Market Running Out of Steam?

After strong stock returns in 2023 and again in the first quarter of 2024, volatility has reared its ugly head in recent weeks. In today’s blog, we want to look at why that has been happening and what we see looking ahead.

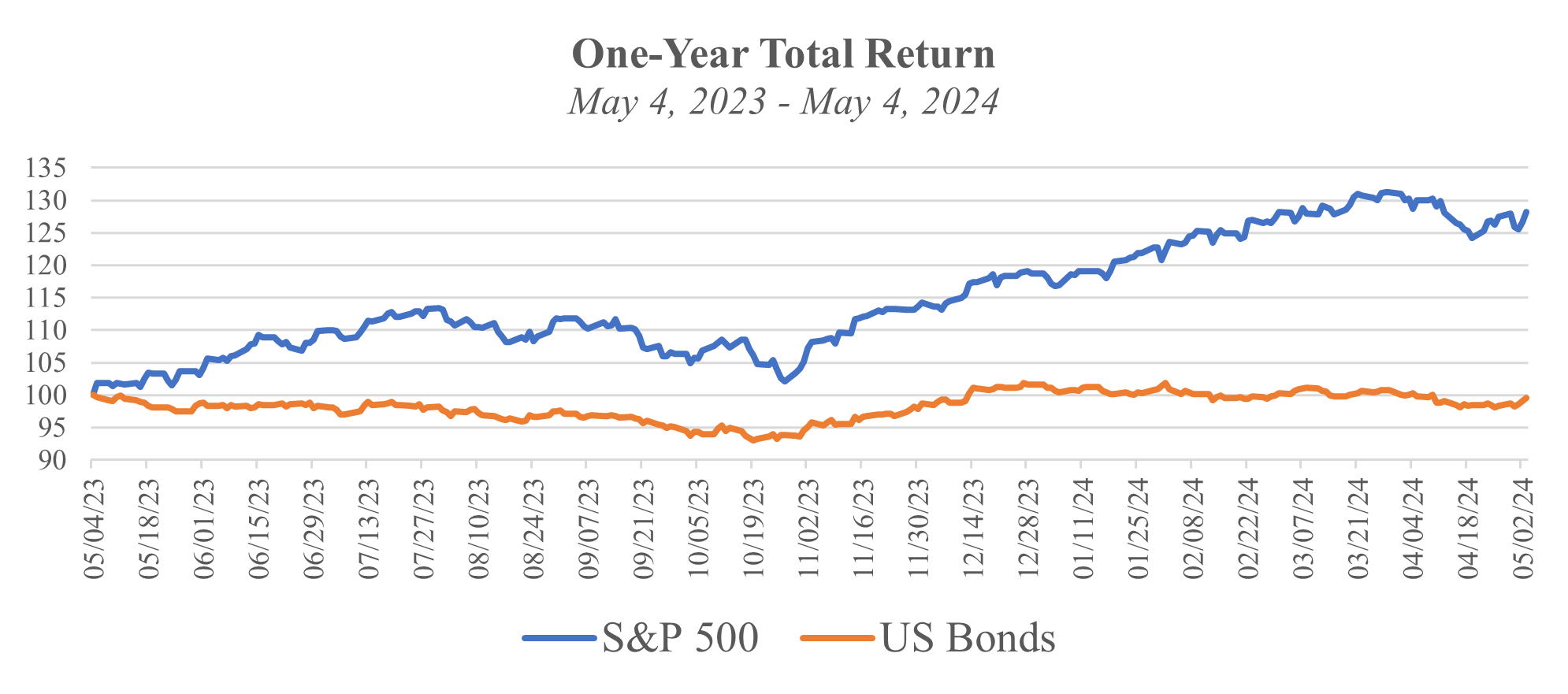

Over the past twelve months, the S&P 500 index has increased by 28% while bond prices have fallen by 0.5% - quite a big difference.

Source: FactSet Research Systems, Archer Bay Capital LLC; Proxy for US Bonds = Bloomberg Bond Aggregate

Two of the biggest factors driving this difference in performance have been the impact of persistent inflation on bond prices and the change in corporate earnings expectations for stocks.

First, let’s look at the impact of inflation on the bond market -

Inflation Since the Pandemic

Source: FactSet Research Systems; US Bureau of Labor Statistics; Archer Bay Capital LLC

The good news is that the inflation rate fell from its peak of 9% in June 2022 to 3% in June 2023. The bad news is that since then, it has vacillated between 3.1% and 3.7%, landing at 3.5% in the most recent report (March 2024).

The Federal Reserve targets inflation at 2% and, to date, it has remained stubbornly above 3%, despite the Federal Reserve’s aggressive interest rate hikes beginning in 2022 in order to bring it down.

As a result of higher inflation, the yields on bonds have moved up with the expectation that interest rates will remain higher for a longer period of time in order to bring down inflation. In the graph below, we look at where the yields on US Treasury bonds were a year ago versus where they are today.

Source: Fidelity Investments; Archer Bay Capital LLC

Treasury bond yields are higher across every maturity today (in green) than they were a year ago (in blue). Plus, the shape of this curve is unusual – bonds with longer maturities normally have higher yields than bonds with shorter maturities and currently that is reversed. This tends to happen when bond investors believe that high interest rates in the near-term will fall over time. Many have expected shorter maturity rates to come down as inflation fell; instead, both short- and long-term rates have moved higher.

Higher interest rates usually impact the economy by slowing down demand, which in turn can lower inflation. Higher interest rates have worked -- inflation is down from the peak. But it is not known how long it will take for inflation to reach the Federal Reserve’s 2% target.

While this tug of war continues between inflation and interest rates, we expect bond market volatility to continue.

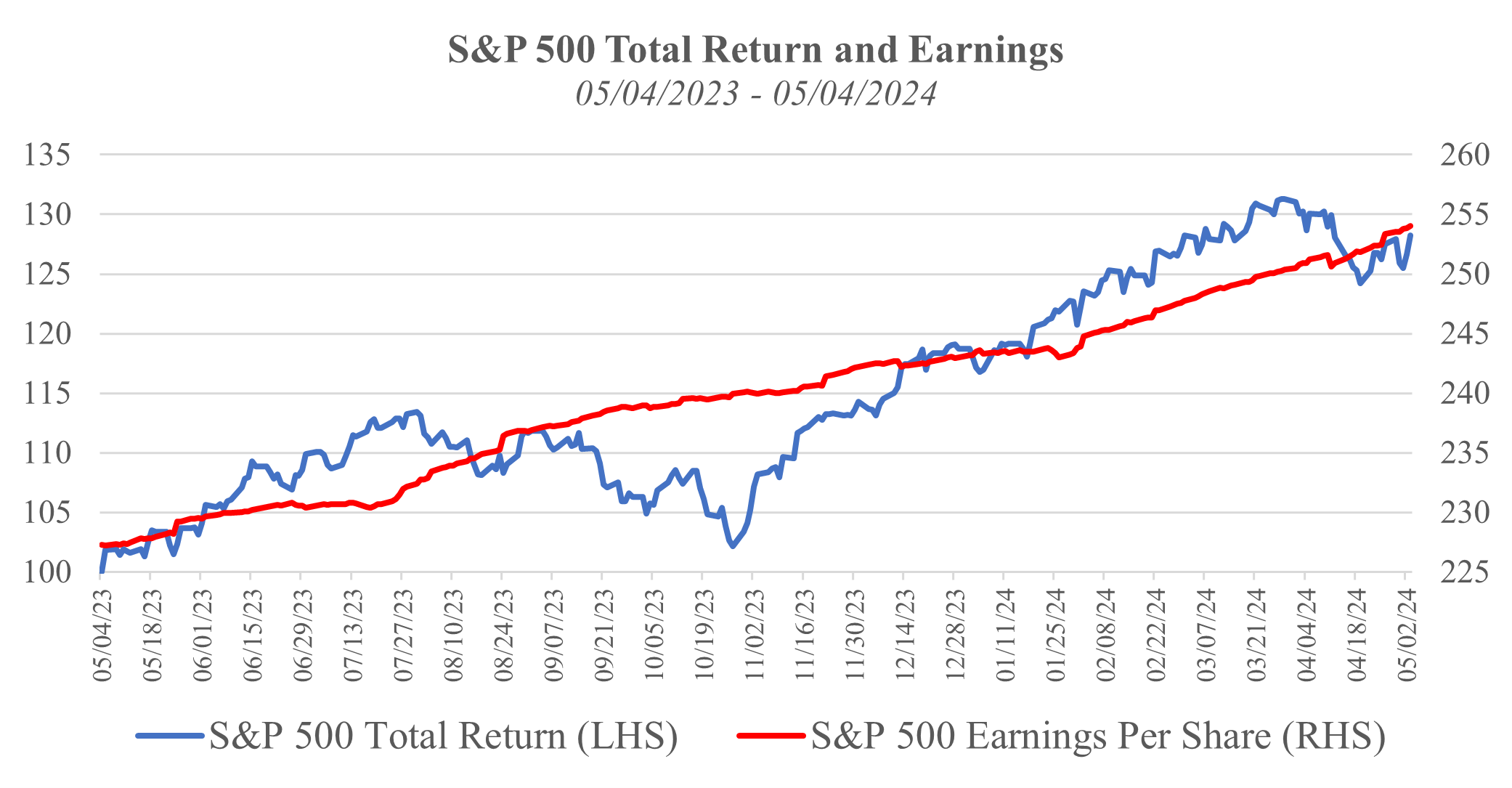

Upside Surprise to Corporate Profits

While inflation has been higher than expected for the past year, corporate earnings have been better than expected.

Source: FactSet Research Systems, Archer Bay Capital LLC

There is a high correlation over time between the performance of the S&P 500 and the aggregate earnings of the companies that make up the S&P 500. The graph above illustrates expected annual earnings over the past year with an overlay of the S&P 500 total return.

The return of the S&P 500 index jumped around a bit, especially last fall when inflation increased unexpectedly, but the increase in earnings expectations has been fairly consistent.

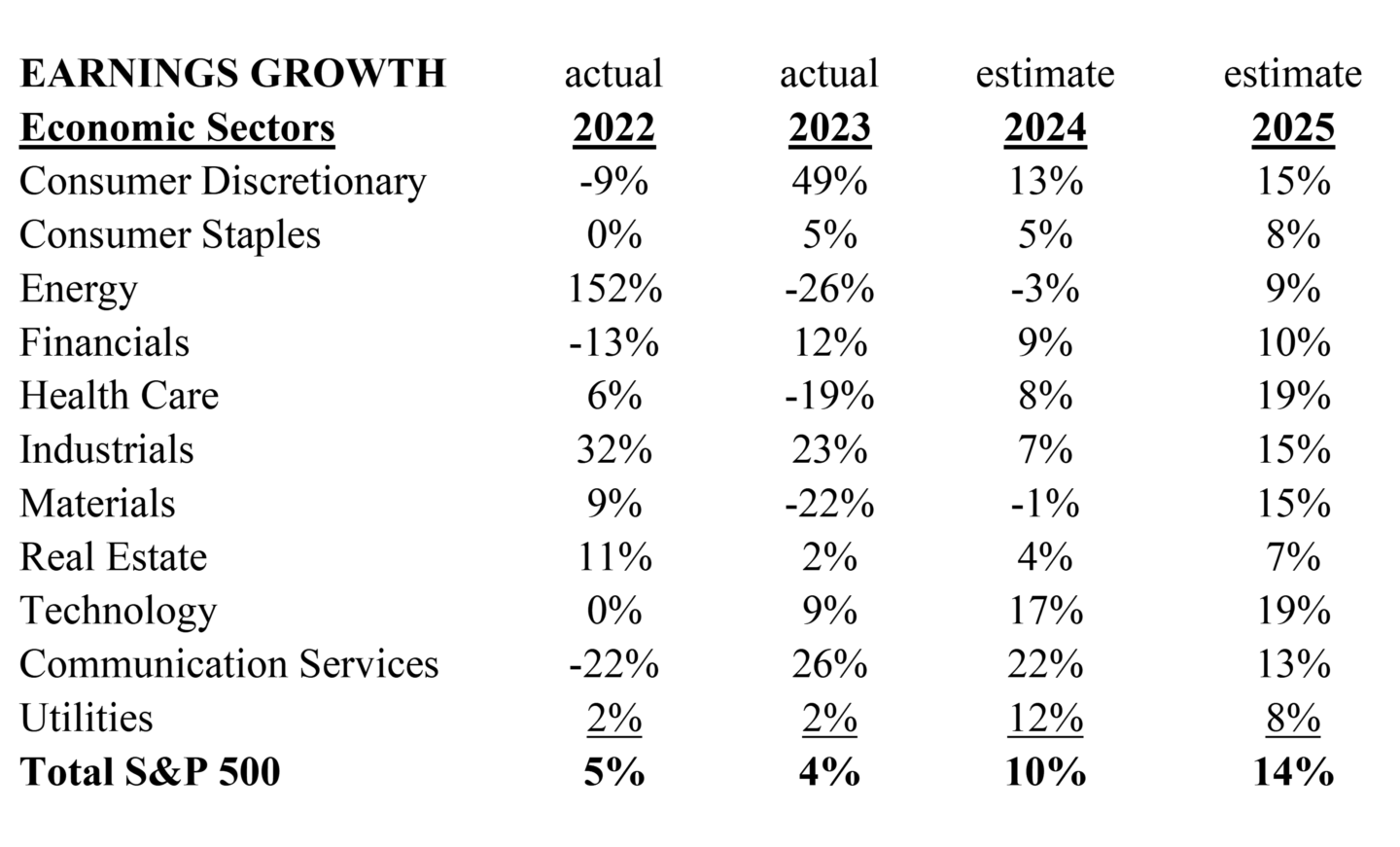

Forward Earnings Expectations Continue to Look Strong

Since the pandemic, earnings growth has been mixed for various economic sectors, while the overall total has been positive. Looking ahead to this year and next, the expectation is for earnings growth to accelerate.

Source: LSEG I/B/E/S; Archer Bay Capital LLC. Earnings growth is based on Calendar Year.

The table above shows the breakdown of the earnings growth rate by eleven economic sectors of the companies within the S&P 500, with the total at the bottom. Wall Street analysts are expecting healthy profit growth across most sectors, which is normal for an economic expansion.

The stock market has been up and corporate profits have been up as well. If inflation continues to decline and the Federal Reserve lowers rates, that will be good for both corporate profits and for the bond market. If inflation remains higher than the Fed’s target, we expect the bond market to continue to struggle and it could be mixed for stocks.

By laddering bond portfolios, we have been able to weather the bond volatility well, primarily because we intend to hold bonds and bond-ladder ETFs until maturity. While the value of the bonds and bond-ladder ETFs may experience some price changes during times of volatility, they drift toward their expected price at maturity over time.

With equities, as always, we stay the course – tracking the long-term positive trend in earnings, especially now as the economy continues to grow.