The Waiting Game

Source: Federal Reserve St. Louis, Federal Reserve NY; Shiller, Yale University; Archer Bay Capital LLC

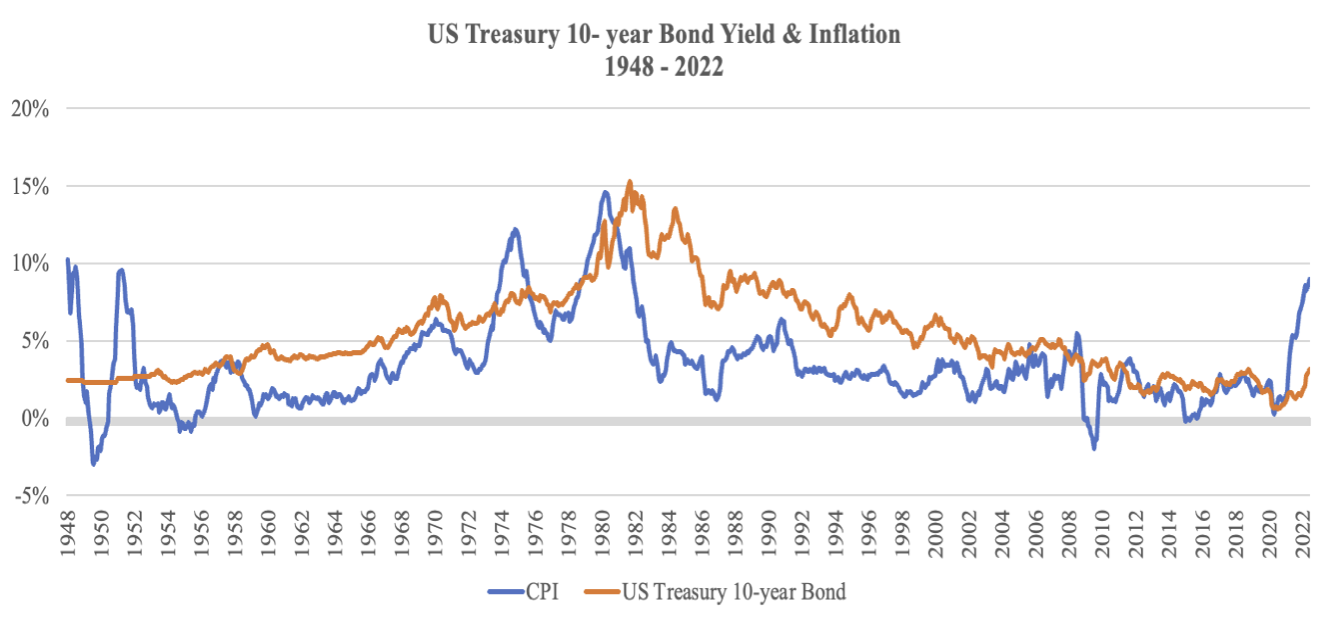

The US inflation rate reached nine percent in June. Energy, food, and housing costs are all up significantly. The economy has been in this position before, but it has been more than forty years since the last inflation shock.

Inflation is measured on a year-over-year basis and we started seeing price spikes in commodities and housing last fall. This means that the headline numbers will likely remain elevated over the next several months until we anniversary those increases.

In some ways, the Federal Reserve and the financial markets are in a waiting game to get through the worst price comparisons. Everyone wants to know how much demand has already fallen due to higher prices. Haven’t we all reconsidered driving trips, grocery choices, and travel when the cost is up so much? It is difficult to gauge demand destruction while it is happening.

The Economy is Slowing

Source: Federal Reserve St. Louis; Archer Bay Capital LLC

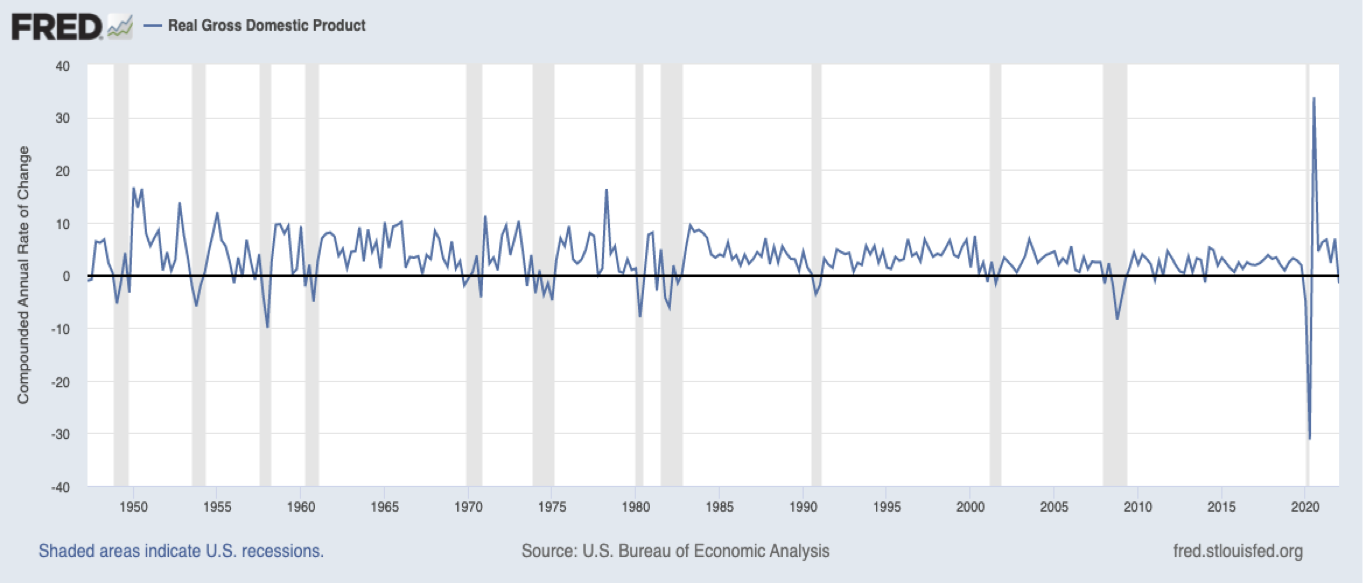

The change in GDP (Gross Domestic Product) for the second quarter (March to June) won’t be released until the end of July, but we know that the first quarter of 2022 was negative. The chart above shows the annual change in GDP every quarter going back to 1948.

It is clear from the chart that the impact from the Covid shutdown in 2020 was the biggest economic contraction that we have experienced since World War II. The government’s response was equally large – the stimulus money got the economy moving again, but at a cost of higher inflation.

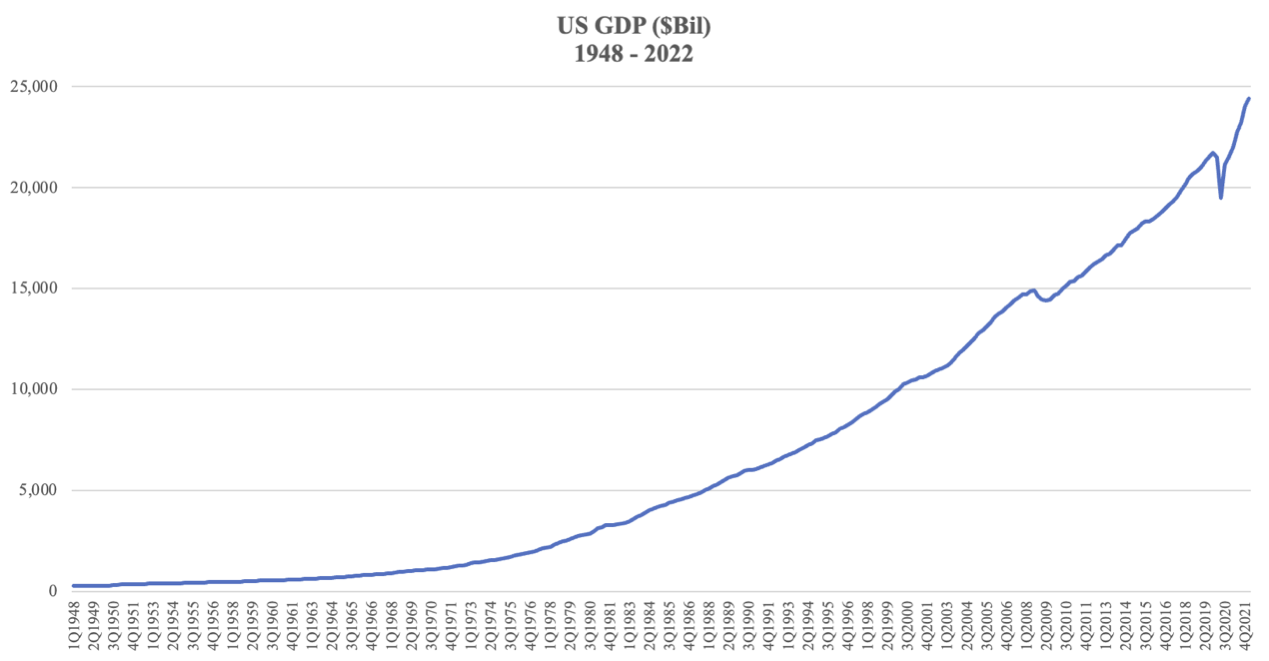

Rather than just looking at the rate of change, it is interesting to also look at the actual economic output of the US. The following chart shows the actual size of the US economy over time – it is now nearly $25 trillion.

Source: Federal Reserve St. Louis; Archer Bay Capital LLC

The US economy has been incredibly resilient. It has grown beyond its size before the pandemic began.

The Bond and Stock Market Response

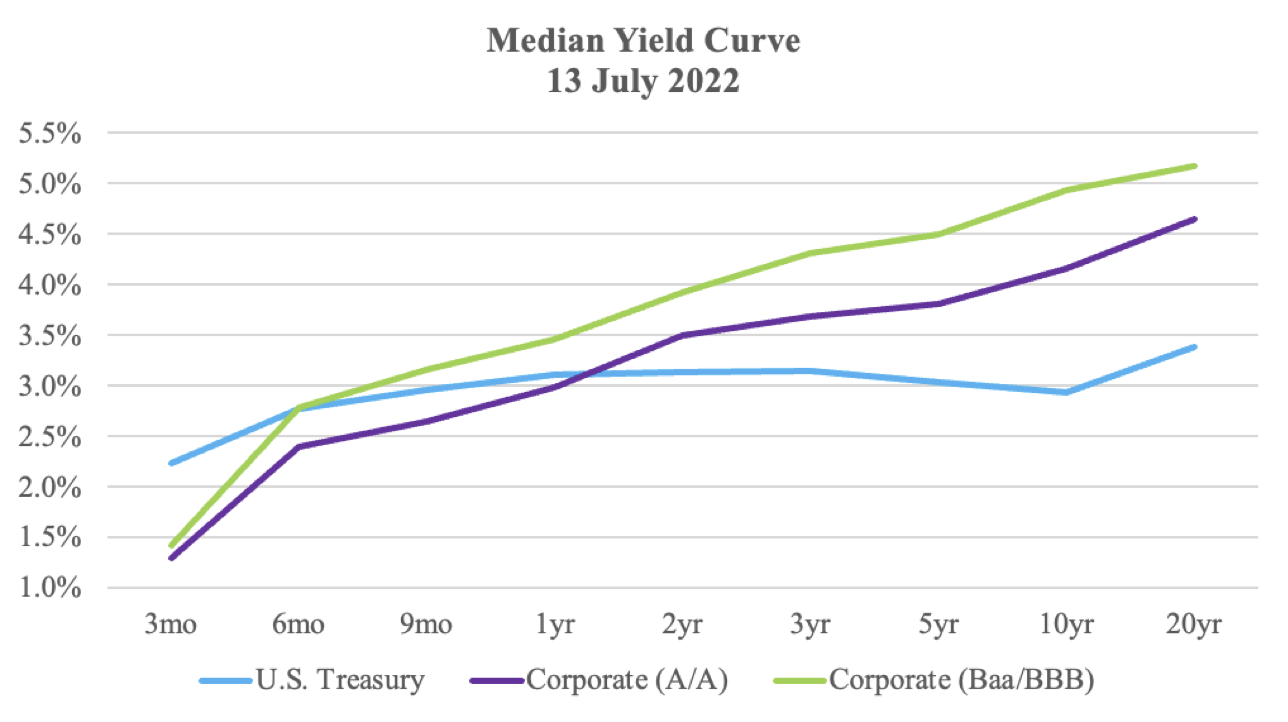

Bond yields have not risen as much as we would expect with inflation so high. The bond market seems to be expecting a recession.

Source: Fidelity Investments; Archer Bay Capital LLC

As we have mentioned before, bond yields are normally higher than the inflation rate. The US Treasury 10-year bond currently has a yield of 2.9 percent...when inflation is at 9 percent. This only makes sense if the economy is contracting.

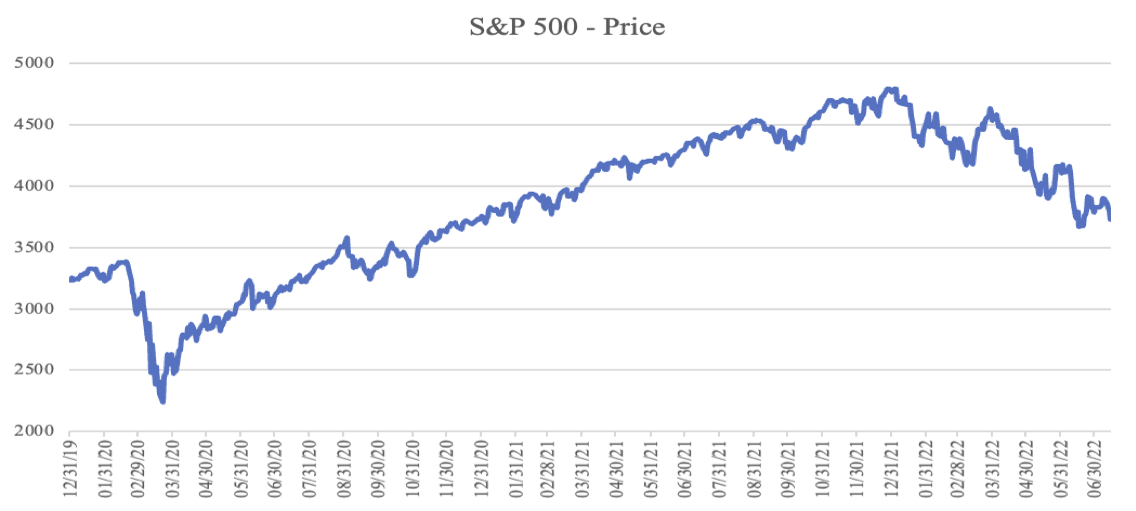

The stock market also seems to be expecting a recession. In the past, stock market declines greater than 20 percent have happened due to recessions. In the chart below, the decline due to Covid is easily recognizable in 2020. The current decline has been more gradual.

Source: FactSet Research; Archer Bay Capital LLC

Given the uncertainty around inflation and economic growth, there could be an additional pullback. The S&P 500 is currently at a fair valuation. Its Price/Earnings ratio is 16, which has been the average for the past twenty years.

Source: FactSet Research; Archer Bay Capital LLC

If we experience a decline similar to what happened during 2020, then there is roughly 10% more downside from here. Based on this data, we think a bottom for the S&P 500 could hit 3500 before a recovery.

Not A Typical Slowdown So Far

If we are in recession, it is a very unusual one. Some things that typically happen in recession are not happening right now. The first is a strong job market.

Source: Federal Reserve St. Louis; Archer Bay Capital LLC

It is very unusual to have low unemployment during a recession. Despite high inflation and a slowing economy, the labor market is tight. We have seen some companies report hiring freezes but very few layoffs, at least not yet.

The second is corporate profit growth.

Source: FactSet Research; Archer Bay Capital LLC

Typically in a recession, companies’ earnings fall, but so far this year, earnings are growing. In aggregate, the companies of the S&P 500 grew their profits 11 percent in the first quarter, despite the decline in GDP. Wall Street analysts are expecting 6 percent earnings growth for the second quarter, and overall profit growth for the full year to be over 9 percent.

In conclusion, we are watching and waiting. Watching the direction of inflation and corporate profits…and waiting for a slowdown in the economy to break inflation. The Federal Reserve is expected to raise interest rates at their next meeting on July 27th, and then again at their following meeting on September 21st. Consumers and business all need relief from higher prices but it doesn’t seem likely before autumn.

Our advice is to enjoy the summer, don’t follow the markets too closely because we don’t expect good news until the fall. We have been through downturns before and stronger corporate earnings always bring the market back.

Please let us know if you would like to discuss in greater detail -- we are always happy to share more in-depth research.